Series A, B, and C Funding: Guide to Raising Venture Capital

Take a look at our comprehensive overview of what you can expect (and look out for) when raising venture capital from Series A to Series C.

Index

Protect your business today

Tell us a little about your business and we’ll create a coverage package that fits your needs, with a price you can count on.

Get a QuoteYou’re likely here because your business is growing rapidly (or you have an idea for a high-growth startup) and you’re interested in getting to the next level by taking on venture investment.

You may have already raised (and spent) money from family and friends — possibly an angel investor — or you’ve bootstrapped the business without any external capital.

Now, you must have a firm understanding of the venture capital ecosystem and prepare yourself for an arduous process: introductions, pitches, negotiations, term sheets, and all the intricacies that go with each stage and every round.

While we won’t cover every single detail or edge case in this guide, we do give a comprehensive overview of what you can expect (and look out for) when fundraising from Series A to Series C venture capital.

Is raising Series A venture capital the right path?

Is your company on the growth trajectory to be a billion-dollar business?

If you’re not confident the answer to that question is a resounding “YES,” then venture capital may not be for you.

As Paul Graham, legendary founder of Y Combinator has said, “Don’t raise money unless you want it and it wants you. It might seem fundraising is one of the defining qualities of a startup. Actually it isn’t. Rapid growth is what makes a company a startup.”*

The vast majority of businesses never raise venture funding and either remain a “small business” or bootstrap their way to becoming a big business. If you’re confident your business is ripe for venture capital, then continue reading to gain a firm understanding of raising Series A, B, and C venture capital.

What is a seed financing round?

Acorns become oak trees.

Typically when a business is in the idea stage (pre-product) or early product development stage (pre-traction), the team raises a seed round of funding.

The seed stage investment, like the Series A and other later stage investments, is a type of equity-based financing. After any round of equity-based financing, investors own shares in the company at negotiated terms.

Seed money is used to get from the idea stage to finding product-market fit. Seed funding is often not enough to get a business to profitability but is a way to reach the next funding milestone: Series A.

Series A funding: just another investment?

Series A is the first step to get to the major leagues of venture capital.

Early stage businesses often raise tens of thousands of dollars from friends and family or hundreds of thousands of dollars from angel investors, but VCs usually seek to invest millions of dollars.

In fact, the average Series A funding in 2018 was more than $11 million.*

Venture capitalists are reliant on their portfolio companies to create value in a step function progression — put another way, to create exponential returns on investments.

When to raise the Series A

Let’s start with the cold hard truth: there are no distinguishing factors for when a company is ready to raise their Series A.

For SaaS companies, many investors look to annual recurring revenue (ARR) as their north star metric to determine when a company is ready to raise. Some investors argue that when a company passes $1 million in ARR they’re ready for their Series A.

In a survey of venture capitalists, the mean ARR requirement was $1.4 million, but the minimum was $600,000 and the maximum was $3 million. This means that the probability of a company being ready (and able) to raise their Series A follows a Gaussian bell curve.* Simply put, neither a low or high ARR is the determining factor for VCs.

How to find the right VCs

When searching for the right venture capitalist, you ultimately need to think about the entire VC firm. What are the firm’s core competencies and areas of conviction?

When the time comes for an in-person meeting (and a second meeting, if you’re lucky) you’ll likely meet with multiple partners. What’s more, you may interface with only junior-level associates. Although associates are not the ones ultimately cutting checks, they may be your biggest advocates in the firm, so show respect to everyone there.

Some things to pay close attention to are conflicts of interest. If the VC in question has conviction in the industry your business seeks to serve, do they already have investments that could be considered competitors?

First Round Capital’s Bill Trenchard advocates founders “scan their [the VC’s] portfolio for similar business models regardless of sector. If you’re selling to SMBs and many of the firm’s companies do as well, the VC could be a good fit.”*

Platforms have emerged to connect the supply of VC capital and entrepreneurs. For example, VCs can be found on Crunchbase or Signal by NFX.

How to get a warm introduction

“Unfortunately, most cold emails aren’t very compelling.” – Sarah Guo, Greylock Partners*

Most VCs expect a warm introduction before they will even consider meeting with an entrepreneur. Some argue that networking is a skill all entrepreneurs must be proficient in to succeed, so warm introductions are a test.

The best introductions come from other investors or entrepreneurs the VC trusts. A cold introduction to a founder who has worked with the target VC is better than a cold email directly to the VC, so start networking.

Find a venture-funded startup succeeding in your industry and research the active partners who made the investment. Get involved in the community on Twitter, LinkedIn, or at a local Meetup.

How to think about the pitch deck

The pitch is rarely a monologue, and the pitch deck is meant to be used as an agenda for the conversation.

Some investors would rather talk everything through than sit quietly and listen to your pitch. If there’s no structure to the conversation, however, important metrics will be overlooked which could result in the investor passing on you. There are some strategies to overcome this situation:

- Bring multiple presentation formats. Before the meeting, send two decks — a “teaser deck” that covers everything at a high level and a full pitch deck that gets into the details. Ask the investor which deck they’d prefer to hear.

- Print copies of the deck for reference. If the VC insists on a fireside chat format, pass out printed versions of the deck and reference it as your agenda to keep the conversation progressing.

Although this section won’t go into details of what metrics and talking points you should include in your pitch deck, there’s something you shouldn’t include: vanity metrics.

Vanity metrics are those that have no measurable impact on the business and only serve to inflate the ego of the person reporting the metric. This can be the raw number of downloads, without retention data, or the founder’s rank on Forbes 30 Under 30. Unless those downloads resulted in daily active users or the 30 Under 30 directly resulted in important hires, the investor doesn’t care.

One final note on the pitch deck: Have a designer format the deck to make it polished. It’s worth showing VCs that you’re dedicated to aesthetics and user experience.

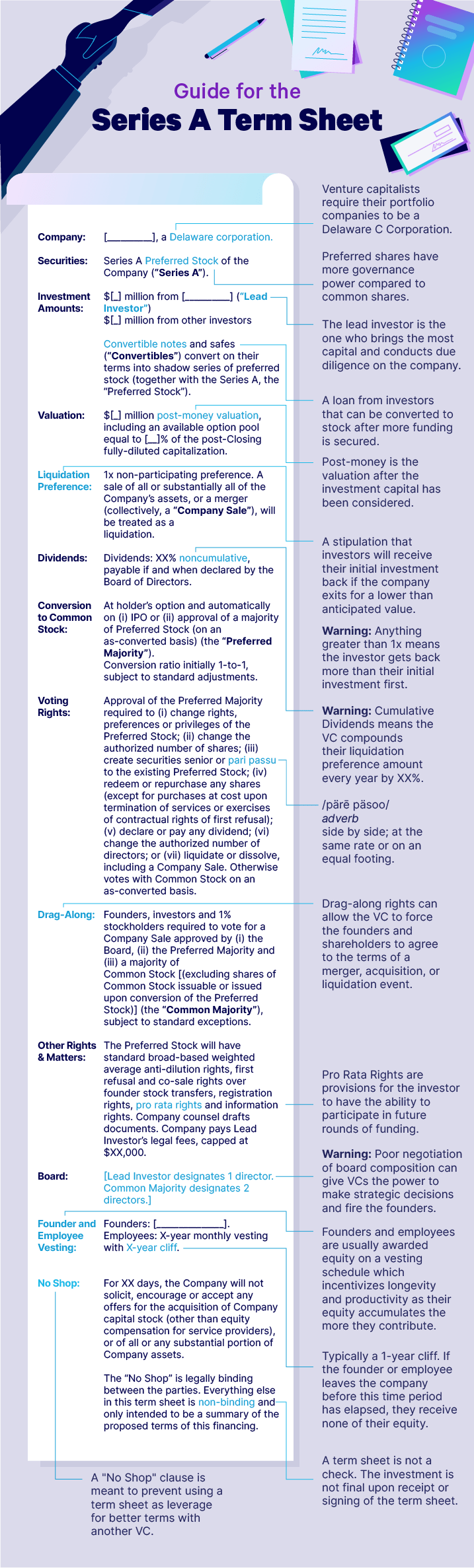

Term sheet 101: Series A

Term sheets should be standard and simple — sometimes simple enough to fit on a single page.* A one-page term sheet may seem innocuous at first, but these terms will be binding throughout the life of your business.

In today’s ecosystem, any legalese that feels out of place or dishonest is a huge red flag for everyone involved.

Below are some details of what will likely be included in the term sheet you’re offered by the VC:

Series A preferred stock

Preferred stock is what venture capitalists, well, prefer.

Preferred shares come with no inherent voting rights, instead they often come with a greater claim to a company’s assets in a liquidity event, and sometimes annual dividend income. Common stocks, on the other hand, have voting rights but have less claim to financial returns compared to preferred stock.

Preferred stock has senior rights compared to common stock, such as the ability to exercise options at a significant discount to the preferred stock price. For example, let’s assume a company issues preferred stock to investors at $1.00 per share. The preferred stock could be converted to common stock before an IPO at a substantial discount to market value.

Some companies opt to have special classes of founder stock to leverage enhanced voting rights and liquidity. Larry Page and Sergey Brin of Google and Mark Zuckerberg of Facebook are famous for the structure of their ownership.

For example, Facebook has a dual class structure that weights different shares compared to others. Facebook’s Class B shares have 10 votes per share and are primarily owned by Zuckerberg and a select group of trusted insiders.

Liquidation preference

A liquidation preference is a stipulation that investors will receive their initial investment back if the company exits for a lower than anticipated value.

If liquidation preference has not been included in the term sheet and the company sells for less than its valuation on the private markets, the investors can actually lose money while the founders get compensated.

Fred Wilson, a longtime venture capitalist at Union Square Ventures, discusses the importance of liquidation preferences as it seems only fair that investors should be returned their investment if the founders are enriched.*

Compensation of the board and employees

This is one of the more controversial topics to discuss (or debate) between the entrepreneur and potential investor.

Investors may request the option pool be included in the pre-money valuation which would further dilute the entrepreneur’s equity in their own company. Let’s use a hypothetical example: Series A investors include a clause in the term sheet for a 10% option pool to be fully diluted post-money.

In the case of a $2 million post-money valuation, the option pool would be equivalent to $200,000. That’s a lot of equity removed from the entrepreneur’s portion of the cap table.

The typical option pool for future employees and board members is 10–15%.

Michael Berolzheimer, founder of the pre-seed stage investment firm Bee Partners cites, “how the option pool impacts founder dilution,” as the biggest term sheet red flag missed by most entrepreneurs, and that all too often, “founders will accept the investors’ recommendation instead of thoughtfully analyzing their ‘option budget’ for the next cycle of hiring.”*

Voting rights

One of the decisions in terms of long-term impact is voting rights for preferred shareholders compared to common shareholders.

This stipulation can grant investors the ability to vote on the affairs of the company, including the power to issue more shares (which can be dilutive to founders), elect a certain number of directors (along with the power to remove/replace board members), and more.

If you make a deal with the wrong investor, you could soon be stripped of your power to operate your own company and/or diluted beyond the point of ever receiving an attractive return on your sweat equity.

Drag-along rights

A provision within the term sheet for drag-along rights allows the investor to force the founders and shareholders to agree to the terms of a merger, acquisition, or liquidation event. These rights are typically reserved for situations when the long-term vision of the founders is not agreed upon by the investor.

The founder may wish to reject a letter of intent (to acquire their company, for example) but even if the terms of the acquisition fall below the valuation, investors may turn to a vote. It usually doesn’t take much of a majority (51%) to approve the deal.

Drag-along rights are not ideal for the entrepreneur but in many cases, they lack the leverage to negotiate these out of the term sheet.

BONUS: Convertible notes and the Series A

A convertible note is a loan from investors — usually during the seed round — that can be converted to stock after more funding is secured, often during the Series A.

Entrepreneurs benefit from this structure by not giving up any equity or voting rights during the early stages of the company, allowing them to operate unobstructed.

The investor receives a substantial discount on price when the stock is converted, which rewards them for the risk of the loan. A word of caution regarding the Series A, however: If the valuation is lower than anticipated, the investors are rewarded with the same number of shares in the company, but at a lower valuation, they now have more ownership and power. Founders must weigh this risk before raising venture capital.

Due diligence

Due diligence is the discovery process investors use to uncover general or professional liabilities, weaknesses, or threats that could materially impact the investment’s ability to return a profit. It’s important that entrepreneurs remain transparent throughout this process and respond to any requests for due diligence documentation promptly.

Many investors, especially in the early stages such as the Series A, will scrutinize the background of the founding team and seek to poke holes in the metrics discussed, such as revenue figures, potential deal flow, etc.

Investors also scrutinize the product by using it for themselves and talking with actual customers. This can reveal insights into whether the product is a pain killer for customers or merely a vitamin.

It’s essential that entrepreneurs present any pending lawsuits, patent infringement, disgruntled employees, or more red tape for consideration by the investors. If you inflated revenue figures or misrepresented the number of active users on your platform, these will all be brought to light in due diligence.

When asked what part of the fundraising process most deals fall apart, Brendan Dickinson of Canaan Partners said, “investments fall apart in the eleventh hour because the investor has lost faith/trust in the CEO. Big surprises in disclosures or other things that can come out in back channel references that weren’t addressed head on.”

Dickinson argues its, “better to hit these things head on.”*

D&O insurance

An often overlooked and underrepresented concern when raising venture capital is directors and officers insurance.

D&O insurance can protect against suits brought by investors for a breach in fiduciary responsibility, by employees for failure to comply with workplace laws, and by customers for a lack of corporate governance.

This protects the directors and officers from personal prosecution in matters of the company. If the company files for bankruptcy, for example, the directors and officers of the company won’t be personally responsible for the debts of the business.

When considering D&O insurance or any other startup insurance, consult Embroker’s startup program with a simple application, instant quotes, customized coverage, and more.

Series B funding

If you’ve already raised your Series A and will require more capital to reach your goals for growth, Series B is your next milestone. The average Series B funding amount in 2018 was more than $24 million, at a valuation between $30 and $60 million.*

Investors in a Series B, unlike the Series A, will be much more interested in the growth rate and actual historical performance, something that likely did not exist in the early foundations of your business.

In fact, more than 34% of investors expect their portfolio companies to grow three times within the 12-month period following the investment. Annual recurring revenue is the metric of choice for most investors in the Series B.

Although it’s not impossible to raise a Series B pre-revenue, it’s highly unlikely, which we’ll cover below.

Raising the right amount

Unless you’re on track to become the next billion-dollar unicorn, then raising a Series B might prove difficult.

The level of investment required combined with your increased monthly burn rate since your Series A makes this round of investment even more stressful and time-sensitive. This is why you must raise the right amount.

Understanding how your free cash flow and revenue growth compare to your current monthly expenses and projected expense growth into the future is essential to survival. Most investors understand that raising 18 months of runway — the length of time you have before the business takes off (or aborts takeoff) — is standard.

18 months of runway gives you 12 months to reach your growth metrics and if more funding is required, you have six months to raise another round.

Down round or flat round

A down round is when the company raises at a valuation less than investors paid in the previous round of funding. This usually happens when the company is desperate for a capital infusion but has less than stellar growth metrics.

A flat round, as you may have guessed, is when the valuation remains the same from the previous round of funding.

In down or flat rounds, the new investors receive a discount on both the price of the equity (since the valuation has remained unchanged or diminished) and the risk of investment (since the company has had more time to prove their ability to release product and acquire paying customers). This also negatively impacts current shareholders, as the market price for their shares, although still private, has diminished.

Series C funding

When raising a Series C, the business has already navigated a few rounds of funding and previous term sheets are met with new term sheets which can have repercussions.

The average Series C round results in $50 million in funding at a valuation between $100 and $120 million. This level of investment brings a new echelon of investors to the negotiating table, including private equity, hedge funds, and late-stage VCs.

Round leader

Even in a VC syndicate, which allows more investors to participate in a round of funding, there’s a lead investor. The lead investor is typically responsible for taking charge of meeting with the leadership team, conducting due diligence, and otherwise vetting the potential for a successful investment.

Finding a lead investor in a Series C can become difficult when your previous investors don’t have enough chips on the table to meaningfully participate in the round. If your previous investors typically wrote checks for between $2 and $5 million, they won’t be able to lead a round of $50 million.

But this doesn’t mean your previous investors won’t be able to contribute to the round at all, and in fact, they may have the right to do just that, which is the subject of our next discussion: Pro-rata.

Pro-rata rights

Pro-rata is the investors right of first refusal to invest in future rounds. Although some may disagree, it’s only fair that your early supporters at least have the chance to participate in doubling down on their investment.

Some investors absolutely require pro-rata rights in their term sheet, and many VCs have raised additional funds specifically to participate in these later rounds. Typically called opportunity funds, many venture capitalists have made the bulk of their returns from their right to back their winners.

Governance documents

As you move into later stage funding rounds, such as the Series C, you’ll likely need to reorganize your governance documents and board of directors.

Most investors, especially lead investors, require a seat on the company’s board of directors for active involvement in strategic decision making. This will change the composition of the board and, if more heavily weighted in favor of investors, could bring about issues with drag-along rights (discussed in the term sheet chapter) and more.

Vesting schedule

When a company is formed, the founders and employees are usually offered equity on a vesting schedule. This could be a three-year vesting schedule with a one-year cliff. This means if the employee (or founder) in question leaves within one year, they receive none of their equity. As each year passes, however, they’re awarded more shares of what the original amount was.

This can present unique issues in later-stage fundraising. If raising a series C, for example, the company has likely been in business for a few years, which could mean the founders and employees are approaching the end of their vesting schedule.

This means the founding team is approaching a ceiling in their equity compensation, which could lead to burnout or even turnover. This is where a secondary market offers venture capitalists a way to invest in the company while offering the founding team some liquidity.

Raising your next round of venture capital

As you’re now aware, there are many things to consider when navigating the VC ecosystem. It’s important you acknowledge the fact that these VCs are negotiating deals full-time and the entrepreneur likely has the least experience at the table.

It’s also important you have a lawyer review all documents and discuss terms before signing or cashing any VC checks. Don’t forget to cover your bases with the right insurance policy for your business and stay up to date on trends in the VC ecosystem.