A startup’s guide: How to navigate business uncertainty

This guide delves into business uncertainty, and offers examples of growing startups that have thrived during economic instability. Find out more.

Index

Protect your business today

Tell us a little about your business and we’ll create a coverage package that fits your needs, with a price you can count on.

Get a QuoteBusinesses have to adapt to the changing times and the volatility of the market, especially given the events of the past few years. While dealing with business uncertainty can be seen as a hurdle to clear, it can also be a growth opportunity in itself. In this guide, we’ll explore what business uncertainty means, share examples of growing startups that have thrived during economic instability, and offer you practical tips on how to deal with business uncertainty.

What is business uncertainty?

Business uncertainty refers to situations in which businesses face risks that can’t be foreseen or measured. During these times, it may be hard for businesses to predict their performance due to unprecedented or constantly changing events. Changes in the political, technological, economic, and environmental landscape — such as technological advances, data breaches, natural disasters, or new business regulations — can cause business uncertainty.

For example, 2020 was a particularly difficult year for businesses to navigate due to unexpected shifts in the economy and industries as a result of COVID-19.

Businesses have always had to deal with uncertainty to some extent, especially startups. Startups often operate under financial uncertainty even when the economy is stable since they’ve yet to solidify their business model. And since the financial security of a startup depends on investors and venture capitalists, economic disruptions could limit the amount of funding they have access to.

That said, it’s not always possible to predict the consequences of economic fluctuations when it comes to the startup funding environment. In 2021, VC funding in the U.S. hit an all time high of $345 billion. However, in 2023, VC funding only raised $170 billion — less than half that of 2021.

In spite of the uncertainty, there are currently a record number of unicorns in the world, with 1,571 companies worth a combined total of $5.5 trillion.

The four levels of business uncertainty

Business uncertainty can be categorized into four levels based on the degree of uncertainty in a given situation.

Level 1: A predictable future

In level one uncertainty, predictions about key variables affecting a company’s performance can be made with a reasonable level of accuracy. Level one situations are perceived as regular business occurrences, like making investments in stable markets or deciding on franchise locations.

Since the future is predictable enough, business owners can proceed with a dominant strategy based on a single forecast and simple simulations without being too concerned about the uncertainties.

Level 2: Alternate futures

In this scenario, the future consists of a set of discrete outcomes that are mutually exclusive and exhaustive. For example, changes in legislation can result in level two uncertainty, as businesses have to revise plans to ensure legal compliance. Being unable to predict competitors’ strategies also puts businesses in a level two situation.

At level 2, traditional decision-analysis techniques cannot predict the actual outcome, but they can establish probabilities and evaluate the risks and payoffs of different strategies. Businesses can then make decisions based on their level of risk tolerance.

Level 3: A range of futures

Level three uncertainty differs from level two in that businesses can identify a range of possible outcomes. However, they cannot identify a set of discrete outcomes and assign probabilities to them. For example, a company can estimate that the consumer penetration rate could be between 10 and 50 percent, but it can’t determine the exact value. The actual value may also fall outside of the range.

Sources of level three uncertainty could include customer demand for new products, new technology performance rates, or unstable economic conditions.

When facing level three uncertainty, businesses should develop a limited set of scenarios that account for the probable range of future outcomes and create strategies that cover the range of possibilities.

Level 4: True uncertainty

Level four uncertainty is rare, and tends to devolve to lower levels of uncertainty over time. In level four uncertainty, future outcomes cannot be predicted at all — even analysis cannot identify a range of possible outcomes or probability scenarios within that range.

This level of uncertainty is likely to occur in emerging markets, or in markets during and after major technological, economic, or social disruptions. For example, the travel industry could be facing level four uncertainty due to the impact of the pandemic.

Since it’s not possible to develop strategies based on likely outcomes when facing level four uncertainty, leaders have to work backward and define a future scenario based on a set of assumptions that would justify a certain strategy. For instance, deciding on the level of demand that would be reasonable for an R&D investment. It may also be helpful to look at the strategies and performance of analogous markets to test which strategies are the most logical and favorable.

Risk vs. uncertainty in business

The difference between risk and uncertainty concerns the level of control and predictability of a given scenario. Risk can be measured using probabilities and thus controlled through risk management and assessment techniques. On the other hand, uncertainty involves situations with unknown variables and outcomes that can’t be measured and are, therefore, hard to predict or control.

For example, risk is when a company moves its data to the cloud, and uncertainty is when a major data breach compromises the data stored in the cloud.

Businesses must manage risk and uncertainty, but with the right mindset and preparation, risk can be managed, and uncertainty can be a catalyst for new opportunities.

What is the uncertainty advantage?

The uncertainty advantage is a business approach in which business leaders leverage times of uncertainty to launch innovative solutions in order to discover new market opportunities. Contrary to typical risk management strategies aimed at minimizing consequences, the uncertainty advantage is a strategy to create new sustainable ways of doing business in an unstable environment.

According to Frank Knight’s book Risk, Uncertainty and Profit, business uncertainty is necessary for profit — if businesses could predict risks in advance and strategize accordingly, then your competitors could do the same. The uncertainty is advantageous in that it allows businesses to identify opportunities in the midst of disruptive times and use them to gain the upper hand over competitors.

A good example of this is Airbnb’s response to the COVID-19 pandemic.

In early 2020, as global travel came to a halt, Airbnb faced a massive wave of cancellations and a steep drop in bookings. Instead of scaling back entirely, the company pivoted quickly by introducing Online Experiences, allowing hosts to earn income by offering virtual cooking classes, meditation sessions, and other interactive events.

The company also introduced features such as long-term stays to address the shift away from vacation bookings during the pandemic years.

At the same time, Airbnb adjusted its policies to offer more flexible booking and cancellation options, addressing traveler uncertainty.

The uncertainty advantage isn’t only applicable to big corporations — businesses of all sizes and industries can benefit from this advantage if the leadership team approaches uncertainty with resourcefulness and creativity.

Examples of businesses that successfully navigated uncertainty

Some of the most well-known businesses began as startups during the Great Recession of the mid-2000s, including Airbnb, Uber, and Groupon. Their success demonstrates that startups can achieve incredible growth, even during uncertain times.

In light of recent economic uncertainties, particularly concerning tariffs and trade policies in 2025, small business owners are feeling both uncertain about the future and stretched to the limit. Companies are adopting a mix of offensive and defensive strategies to navigate these challenges.

Let’s go over some examples of startups that have successfully navigated business uncertainty and see how they applied these strategies.

FedEx: Consolidate operations

In 2023, FedEx faced significant challenges due to a post-pandemic slowdown in global demand following a boom in online shopping during the pandemic. To navigate this economic uncertainty, CEO Raj Subramaniam implemented a $4 billion cost-saving plan, which included consolidating operations and reducing the workforce by tens of thousands. These measures helped stabilize the shipping company and recover the share price to near-pandemic highs.

3DHQ: Expanding to new markets

3D-printing company 3DHQ identified new market opportunities during times of uncertainty. While the company mainly revolved around 3D-printing figurines, during the personal protective equipment shortage mid-pandemic, the company expanded its operations to produce masks with filters to supply to healthcare workers and hospitals. The company also bought more printing equipment to keep up with the ongoing demand.

To follow in the footsteps of this company, assess whether the technologies and equipment that your business currently uses can be repurposed to create new products to meet the needs of the ever-changing market.

Bizzy Coffee: Diversifying sales channels

Although financial loss is likely during periods of economic disruption, you could find ways to make up for that loss by diversifying your business to other sales channels. When business went down for local coffee chains, Bizzy Coffee was able to grow their business because they had diversified to multiple sales channels — grocery stores and Amazon. In fact, their online sales have tripled and their products have gone from being in 400 stores to about 900 stores.

As this example shows, in the face of uncertainty, diversification can act as a growth strategy and a fallback option if other sales channels are affected.

Talulah Jones: Joining the e-commerce industry

Owners of brick-and-mortar stores may find themselves in a bind due to business closures. Lifestyle boutique Talulah Jones took this opportunity to launch an online shop and double down on social media marketing. By thinking of innovative ways to preserve the quality of in-person shopping experiences, they found success in their customized virtual shopping experiences and drive-thru services.

With the e-commerce industry booming more than ever, now could be the time to go digital to make your products and services more accessible to customers.

Eagle Electronics: Adjusting to regulatory changes

In 2025, Eagle Electronics, an Ohio-based startup, successfully navigated the challenges posed by increased U.S. tariffs on Chinese imports by onshoring production of IoT cellular modules. By licensing technology from China’s Quectel and establishing manufacturing operations in Cleveland, Eagle Electronics has made major moves to reduce reliance on foreign manufacturing. This strategic move aligned with the broader trend of U.S. companies seeking to localize supply chains amid evolving trade policies.

The startups in these examples took varied approaches to navigate uncertainty, some focusing on preserving cash flow, some expanding to new markets, and others pivoting entirely. Learning from startup examples can help you discover strategies that work best for you.

How to navigate business uncertainty

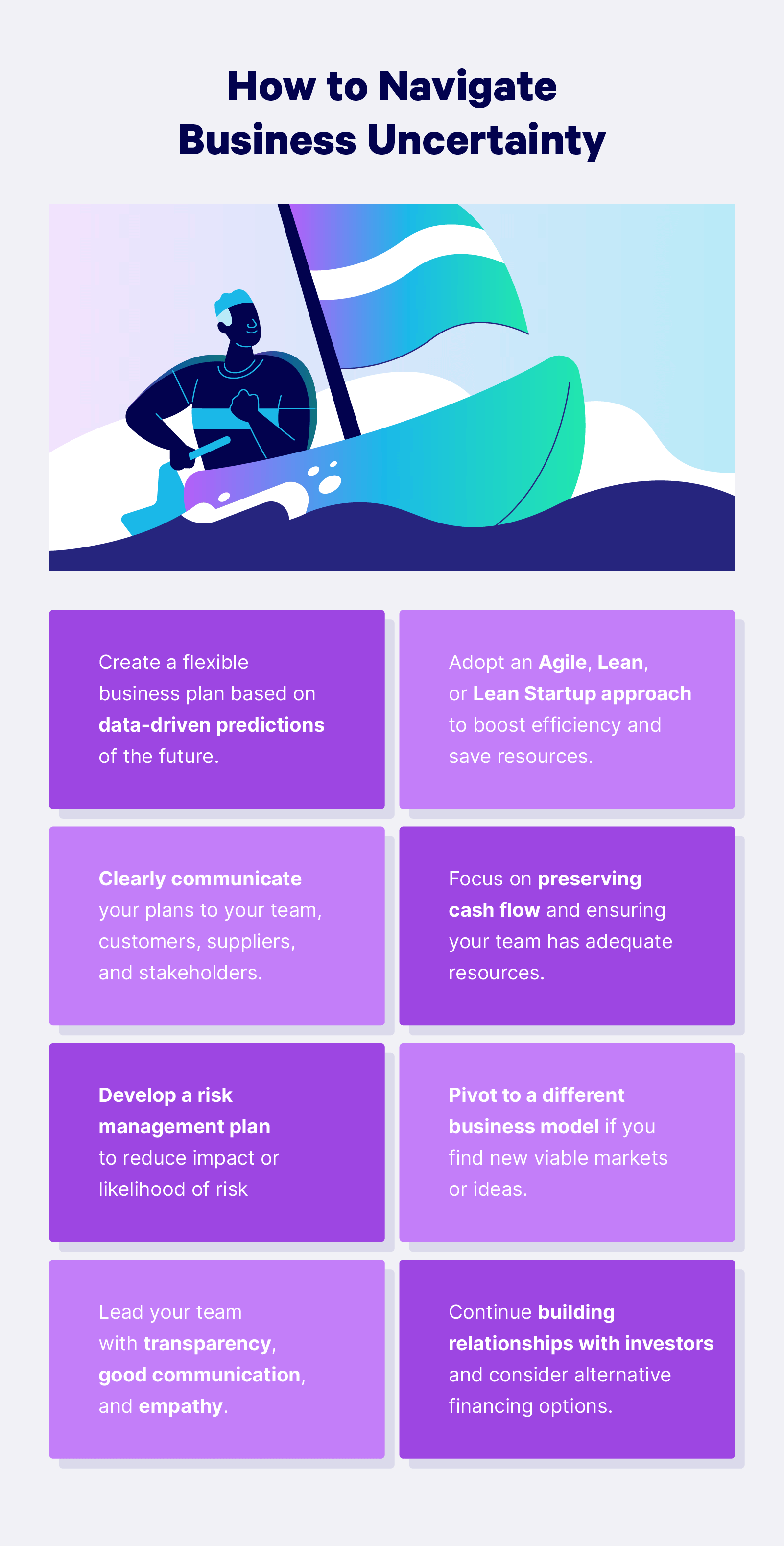

Running a startup involves constantly confronting uncertainty and overcoming challenges. While there’s no one-size-fits-all approach to dealing with business uncertainty, there are general tips that can help you and your team navigate difficult times with more ease.

Develop a dynamic business strategy

In a volatile market, startups should prioritize maintaining a steady cash flow. This means revisiting and revising your current operating plan to make it flexible and dynamic based on the current data available.

The second largest reason for startup failure is running out of funding, so it’s important to stay on top of your finances and keep track of key numbers such as your company’s number of leads, conversion rates, revenue, and profit margins. Calculate your burn rate and monitor your bank balance so that you can make preparations ahead of the “zero cash date” — the projected date when your business will run out of money.

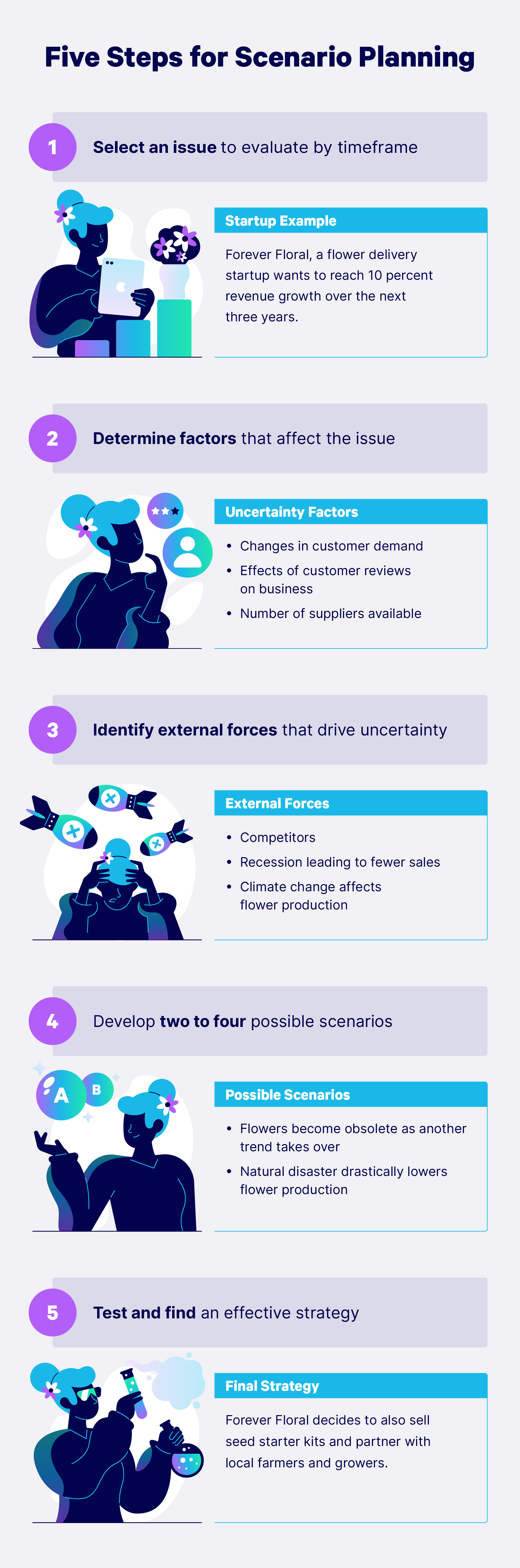

To develop a sound plan that covers various possible outcomes in an uncertain environment, use scenario analysis to define a set of possible futures based on anticipated challenges. Then, develop strategies to respond to each scenario.

Test your revised business plan in the markets and continually monitor to gain real-time feedback. Tweak the strategy to adapt to internal and external changes while keeping an eye on your finances, and test again until you find the most effective plan.

Establishing a dynamic business strategy prepares you to deal with a range of possible scenarios while ensuring you have enough funds and resources to do so.

Stay lean and/or agile

Depending on the type of startup you run, adopting one of these business approaches can help streamline your operations and help you save money:

1. Agile

The Agile approach, originating in the IT world, allows your team to be more adaptive, creative, and resilient when facing change and uncertainty.

Being Agile involves engaging in efficient and continuous cycles of thinking and doing, which means testing products throughout the development process.

For example, to reduce your cycle times, consider shifting to quarterly cycles for planning, doing product sprints to build minimum viable products (MVP), and working in cross-functional teams.

2. Lean

Lean operation is a manufacturing methodology that focuses on minimizing waste while still providing quality products to customers. By streamlining systems, cutting unnecessary costs, and reducing waste, lean companies are able to quickly transition between tasks to increase efficiency, and adapt to the changing needs of customers.

With today’s technologies, you can operate lean by automating systems and standardizing processes.

3. A lean startup

The Lean Startup methodology, coined by entrepreneur Eric Ries, combines the best of the Agile and Lean approaches. It focuses on the question, “Should this product be built?” based on testing the product against the market.

To follow the Lean Startup approach, engage in a build-measure-learn feedback loop by first identifying a problem to solve and then developing an MVP to test in the market. The feedback from the market will then allow you to pivot quickly to another idea, niche, or market if needed.

These methodologies can be applied across different industries, so find the approach that works best for your startup.

Prioritize transparent communication

Effective communication is vital for keeping your company running smoothly during times of uncertainty. Focus on both internal and external communication to ensure that customers, staff, stakeholders, and all parties in the supply chain are kept up-to-date.

Keep your team in the loop by being transparent about the current state of the company and your plan of action. Acknowledge the uncertainties so that the whole team can brainstorm solutions together.

It’s also important to focus on strengthening current relationships with customers to build brand loyalty that will help you weather the crisis. Listen to customers’ needs and think of ways to maintain the same level of quality products or services for them.

You also need to inform your investors and stakeholders of your operating plan and forecasts and be prepared to address their questions. The more clearly you communicate your strategies to stakeholders, the more confidence they will have in your ability to steer the company forward.

Transparent communication is key to building trust in the team and maintaining good client relations when faced with the unknown.

Focus on what you can control

It may be difficult to decide where to focus your attention during uncertain times, so to avoid being overwhelmed, acknowledge the things that are outside your control and focus on what you can control — preserving cash flow, for instance.

Maintain a steady cash flow by ensuring your current client base is satisfied with your company’s products or services, and work on acquiring new customers once circumstances start improving. Find ways to reduce variable costs, such as advertising, and make arrangements with suppliers and vendors to renegotiate contracts if necessary.

By focusing your efforts on variables within your control, you’ll be in a better position to deal with unpredictable variables.

Establish a risk management plan

It’s always better to be as prepared as possible, even when markets are stable, so having a risk management plan can help mitigate consequences when things go wrong.

To create a plan, brainstorm all the potential risks that your business may encounter, be they compliance, operational, financial, or reputational risks. Then, measure the levels of risk based on the likelihood of them happening and the amount of impact they’d have on your business. From there, you can determine ways to deal with the risks by applying one of these four common strategies:

- Avoid the risk entirely

- Reduce the level of risk by taking steps to minimize potential negative impacts or reduce the likelihood of a negative outcome

- Accept the risk as a regular business occurrence and go ahead with the plan

- Transfer part of your risk to an insurance company by buying general liability insurance or insurance plans specific to your industry

While a risk management plan can’t make your startup “disaster-proof,” having a sound plan will definitely help preserve the longevity of your business. Over time, you'll also want to make sure you monitor and update your plan accordingly.

Be flexible and pivot

The upside to business uncertainty is that it can create new opportunities. As you sustain your startup, look for growth, outreach, or marketing opportunities that arise as different industries evolve.

Once you’ve laid out a potential plan and received positive feedback from testing it in the market, commit to the pivot. For example, since the pandemic caused demands to rise in the healthcare industry, many startups found ways to diversify by producing and selling medical equipment.

Embrace the trial-and-error nature of business and experiment with new ideas. Along the way, you might discover a business pivot worth committing to.

Support your team

In times of uncertainty, your team needs a strong leader more than ever. It’s the job of a leader to balance transparency and hope by being realistic with the team while also offering hope by laying out a vision for the future. Acknowledge the challenges and define strategies that will help overcome those challenges.

It’s also important to lead empathetically and show your team members how valued they are. Take time to check up on each team member’s wellbeing, create a flexible and supportive workplace environment, and provide staff with the tools or training they need to succeed. Building a resilient team by overcoming adversity together can bring big payoffs in the future.

Continue looking for funding sources

Access to venture capital is essential to a startup’s survival in turbulent times. Continue pursuing new investments, but also keep in mind that fundraising opportunities may be limited. Reinforce current stakeholder relations by holding shareholder meetings to communicate your forecast for the next few quarters.

If you’re already in the process of fundraising, be flexible when it comes to valuations and be prepared to give more equity as investors may be more risk-averse in an uncertain economy.

Consider alternate funding sources like convertible loans or short-term financing to ensure you have enough funds to last.

Uncertainty is a challenge that all startups face at some point, whether it’s due to changes in the industry, environment, or economy. Business risks can’t always be predicted, but business leaders can best prepare for them by developing strategies that can apply to a range of possible outcomes. Communication, flexibility, and transparency are also key to maintaining valuable business relationships during uncertain times.

Once the right mindset and strategies are in place, the challenges of business uncertainty can be turned into opportunities for growth and innovation.